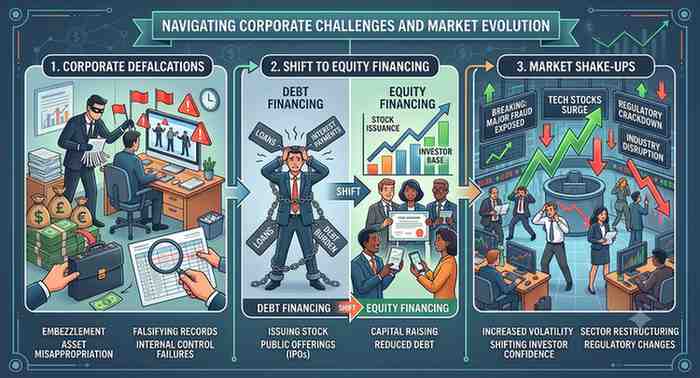

Corporate Defalcations, Shift to Equity Financing, and Market Shake-ups

- Editor

- July 15, 2026

- Uncategorized

- 0 Comments

New Delhi, July 2026 — India’s corporate and startup ecosystem is facing a sharp reality check as funding models shift, market bubbles show signs of straining, and regulatory bodies tighten their grip. From court battles in Singapore to coordinated market manipulation tracking in India, the era of easy money is meeting rigid corporate accountability.

The Udaan Default: The Perils of High-Volume, Low-Margin B2B Scaling

B2B e-commerce platform Udaan has been dragged into a Singapore court by a consortium of lenders, including Standard Chartered Bank and Samena Capital. The lenders are pushing for bankruptcy proceedings and seeking a liquidator to recover funds following a $170 million convertible bond default.

The crisis highlights a structural flaw in the company’s cash-heavy model. Acting as an intermediary between bulk sellers who demand rapid payments and buyers who require extended credit, Udaan faced a crippling cash-flow crunch as it scaled. The convertible bonds were tied to a June 30 deadline, structured around an expected IPO that never materialized. While the Indian operating entity remains legally separate for now, the dispute marks a stark downslide for a firm once celebrated as India’s fastest-growing unicorn.

The Adani Pivot: Trading Debt for Equity

In a major strategic realignment, the Adani Group is systematically moving away from its historically heavy reliance on debt to leverage growth. The conglomerate is aggressively utilizing Qualified Institutional Placements (QIPs) to raise capital through equity instead.

Adani Energy Solutions, which secured ₹8,500 crore via a QIP in May, has now obtained board approval to raise an additional ₹10,000 crore. The funds are earmarked to build an expansive infrastructure pipeline, including the recent ₹350 crore acquisition of IntelliSmart. With Adani Enterprises also planning a ₹3,000 crore QIP, the group’s shift toward selling stakes rather than taking on debt signals a defensive play against high leverage.

The SoftBank Dilemma: The First Crack in the AI Bubble

Signs of an artificial intelligence valuation bubble are hardening as SoftBank faces rigid resistance from global financial institutions. Despite holding a 13% stake in OpenAI valued at over $64 billion, major merchant banks—including Goldman Sachs and JPMorgan—flatly rejected SoftBank’s request to raise cash by leveraging that equity.

The refusal stems from a lack of immediate liquidity, compounded by reports that OpenAI will delay its IPO. SoftBank is now left highly exposed, sitting on a massive $40 billion bridge loan expiring in March 2027. To secure alternative lines of credit, the firm has been forced to offer corporate guarantees alongside its equity, providing concrete proof that institutional lenders are growing highly skeptical of inflated AI valuations.

Data Analytics vs. Pump-and-Dump Syndicates

The Securities and Exchange Board of India (SEBI) has exposed a massive ₹144 crore market manipulation syndicate, issuing multi-year bans and heavy fines across more than 20 entities. The operation targeted small-cap stocks, utilizing over 200 coordinated trading accounts to artificially inflate trading volumes before blasting retail investors with misleading SMS stock tips.

In a highly sophisticated investigation, SEBI blew past the entities’ claims of being unrelated by auditing local consumer data. By analyzing Zomato, Swiggy, and commercial travel records, the regulator proved that the operators routinely ordered food from identical locations and traveled together. Ringleader Hani Sheikh faces a 7-year market ban and a ₹10 crore fine, sending a clear warning to operators manipulating illiquid small-cap stocks.

Bottom Line

Whether it is the liquidity trap of B2B e-commerce, the inflation of AI assets, or illicit small-cap syndicates, the market is aggressively correcting. Corporate growth is no longer being judged by top-line expansion or hype, but by actual cash flow, transparency, and sustainable capital structures.