Why RBI’s Rate Hold Reflects a Calculated Bet on Geopolitical Inflation Risk

- admin

- April 3, 2026

- Uncategorized

- 0 Comments

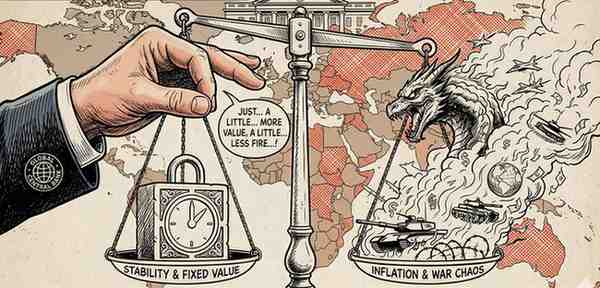

The Reserve Bank of India has maintained its benchmark repo rate unchanged, prioritising inflation vigilance over growth stimulus as West Asia conflict threatens to disrupt global energy markets. This decision signals the central bank’s assessment that imported inflation risks currently outweigh domestic demand considerations in its monetary policy calculus.

New Delhi, April 2026 — The RBI’s Monetary Policy Committee has opted to hold the repo rate steady, marking a deliberate pause that reflects mounting concerns over supply-side inflation pressures emanating from escalating West Asia tensions rather than any fundamental shift in domestic economic conditions.

What Is Driving the RBI’s Decision?

West Asia conflict has introduced significant uncertainty into global crude oil markets, with Brent prices showing elevated volatility over the past six weeks. India imports approximately 85 per cent of its crude oil requirements, making the economy acutely vulnerable to supply disruptions and price spikes originating from the region. The RBI’s inflation mandate under the flexible inflation targeting framework requires maintaining CPI within the 2-6 per cent band, and any sustained crude price surge could push headline inflation toward the upper threshold. Governor Shaktikanta Das and his successors have historically demonstrated heightened sensitivity to imported inflation during geopolitical episodes, notably during the 2022 Ukraine crisis when rates were hiked by 250 basis points cumulatively.

What Does This Mean for India’s Growth Trajectory?

The rate hold creates a holding pattern for credit-sensitive sectors including real estate, automobiles, and capital goods manufacturing. Indian GDP growth projections for FY2026-27 remain in the 6.3-6.7 per cent range, but the RBI’s cautious stance suggests the central bank sees inflation management as the prerequisite for sustainable expansion. Small and medium enterprises, which rely heavily on bank credit, will continue facing elevated borrowing costs that have persisted since the post-pandemic tightening cycle. Consumer spending patterns may moderate further as household budgets absorb both existing EMI burdens and potential fuel price pass-throughs.

How Does This Compare Globally?

The RBI’s approach aligns with the cautious posture adopted by several emerging market central banks facing similar external vulnerabilities. Brazil’s Banco Central and Indonesia’s Bank Indonesia have similarly paused rate cuts despite softening domestic inflation, citing geopolitical commodity risks. The US Federal Reserve’s own rate trajectory remains uncertain, limiting the RBI’s room for aggressive easing without risking rupee depreciation and capital outflows. India’s real interest rate differential with developed markets remains a key consideration for foreign portfolio investment stability.

- Repo rate held at current level; no change in reverse repo or standing deposit facility rates

- India imports 85% of crude oil, making it highly exposed to West Asia supply disruptions

- CPI inflation targeting band remains 2-6%, with current readings within tolerance

- Previous geopolitical-driven tightening cycle (2022) saw cumulative 250 bps rate hikes

- FY2026-27 GDP growth projected at 6.3-6.7%, contingent on inflation stability

What Should Investors Watch?

Fixed income investors should monitor the 10-year government bond yield curve for signals on market inflation expectations and fiscal consolidation progress. Equity market participants, particularly in rate-sensitive banking and infrastructure sectors, must track weekly crude price movements and any escalation indicators from West Asia. Currency traders should watch RBI forex intervention patterns, as rupee stability will influence the central bank’s comfort level with any future rate adjustments. Corporate treasury managers across import-dependent industries should consider hedging strategies against potential rupee depreciation scenarios.

Analyst’s View

The RBI’s rate hold represents prudent risk management rather than policy paralysis, acknowledging that monetary tools have limited efficacy against supply-driven inflation shocks. The central bank appears to be preserving policy ammunition for a scenario where West Asia tensions either escalate dramatically or resolve, enabling a clearer directional move. Market participants should anticipate an extended pause lasting at least two more policy cycles unless crude prices stabilise below $80 per barrel or conflict de-escalation becomes evident. The RBI’s next inflation projections and any revisions to its risk assessment framework will provide the clearest forward guidance on when the current holding pattern might shift toward accommodation.