Iran Conflict Reshapes Global Commodity Flows: Oil, Food and Capital Markets Face Structural Realignment

- admin

- April 2, 2026

- Uncategorized

- 0 Comments

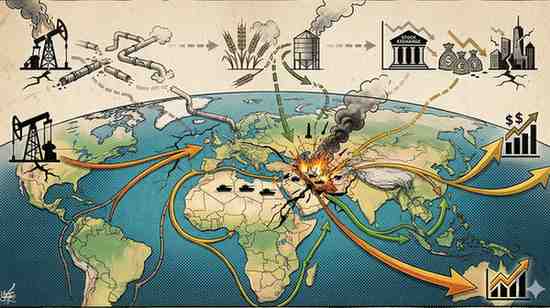

A month of sustained military conflict involving Iran has fundamentally disrupted global commodity supply chains, triggering oil price surges above $120 per barrel, wheat futures spikes of 40%, and a flight to safe-haven assets that has redrawn capital allocation patterns. The economic fallout extends far beyond the Persian Gulf, with emerging markets facing acute import cost pressures while commodity exporters experience windfall revenues that mask deeper structural vulnerabilities.

New Delhi, May 2025 — The Strait of Hormuz, through which approximately 21% of global petroleum consumption transits daily, has become the epicentre of a supply shock not witnessed since the 1973 Arab oil embargo. Shipping insurance premiums for Gulf-bound tankers have increased sevenfold since hostilities commenced, effectively pricing out smaller trading firms and consolidating cargo flows among a handful of major shipping conglomerates willing to bear conflict-zone risk.

What Is Driving Global Market Disruption?

The Iran conflict has created a three-pronged economic shock operating simultaneously across energy, food, and financial channels. Brent crude prices crossed $125 per barrel in the third week of fighting, representing a 55% increase from pre-conflict levels. Russia and Saudi Arabia have declined to release substantial strategic reserves, calculating that elevated prices serve their fiscal interests despite Western diplomatic pressure. The International Energy Agency has coordinated a 60-million-barrel emergency release from OECD strategic reserves, but this intervention has merely slowed price acceleration rather than reversing the trend.

What Does This Mean for India?

India’s economy faces disproportionate exposure given its 85% dependence on imported crude oil and significant wheat import requirements following below-average domestic harvests. The Reserve Bank of India’s inflation trajectory has been upended, with April wholesale price index readings suggesting headline inflation could breach 8% by June. The rupee has depreciated 6.2% against the dollar since conflict commenced, compounding import costs and forcing the RBI to intervene with approximately $18 billion in forex reserves. Current account deficit projections for FY26 have been revised upward from 2.1% to an estimated 3.4% of GDP by multiple investment banks.

How Does This Compare to Previous Oil Shocks?

The present disruption differs structurally from the 2022 Russia-Ukraine energy shock because it directly threatens physical chokepoint transit rather than merely sanctioning one supplier. The 1990 Gulf War provides a closer parallel, when oil prices doubled within three months before coalition forces restored Kuwaiti sovereignty. Global financial markets in 2025, however, are far more interconnected than in 1990, with algorithmic trading amplifying volatility and contagion spreading instantaneously across asset classes.

- Brent crude: $125.40 per barrel, up 55% from pre-conflict baseline of $81

- Strait of Hormuz traffic: down 34% as shippers reroute via longer Cape of Good Hope passages

- CBOE Volatility Index (VIX): sustained above 32, indicating persistent risk aversion

- Gold prices: $2,890 per ounce, a record high reflecting safe-haven demand

- Global shipping rates (Baltic Dry Index): up 28% on route diversions and vessel scarcity

What Should Investors Watch?

Three indicators merit close monitoring over the coming weeks. First, Iran’s crude export volumes to China and India will signal whether Asian buyers are defying Western pressure or complying with tightening sanctions. Second, US Strategic Petroleum Reserve drawdown pace will determine how long Washington can suppress prices before exhausting intervention capacity. Third, central bank policy responses in emerging markets will reveal whether monetary authorities prioritise currency defence or growth support.

Analyst’s View

The Iran conflict has exposed the fragility of globalised supply chains that assumed perpetual freedom of navigation through contested waterways. Structural repricing of geopolitical risk premiums is underway across commodity and currency markets, and this repricing will persist regardless of how hostilities conclude. Indian policymakers should anticipate a protracted period of elevated import costs and calibrate fiscal responses accordingly, particularly regarding fertiliser and fuel subsidies. The global economy has entered a phase where security considerations will increasingly override efficiency optimisation in supply chain design, with lasting implications for inflation dynamics and capital allocation.